UK Casino ID Verification Checks and Fast Withdrawal Rules

Related account guides: full overview, check the business first, bonus and balance terms, ID document and privacy risks, complaints and dispute route.

Índice de contenidos

- Clear Steps for UK Casino Payment and Withdrawal Issues

- Decision path for payments, ID and withdrawals

- Payment-method checks

- Age, identity and financial checks

- Withdrawal problems: what is useful to ask

- Warning signs to take seriously

- When pressure to gamble is part of the issue

- Official pages that support these checks

- Payment, ID and withdrawal decisions

Clear Steps for UK Casino Payment and Withdrawal Issues

Before deciding whether something is ordinary, unfair or risky, name the issue precisely. Is it about a payment method? Is the site asking for age or identity documents? Is it asking about income, bank statements or other financial information? Is a withdrawal delayed? Or is a bonus balance being treated differently from a deposit balance?

Those questions lead to different checks. A payment-method issue is not the same as a document-safety issue. A source-of-funds request is not the same as a bonus restriction. A withdrawal delay is not automatically proof of wrongdoing, but it should have a clear explanation and should not be used to create unreasonable pressure.

Decision path for payments, ID and withdrawals

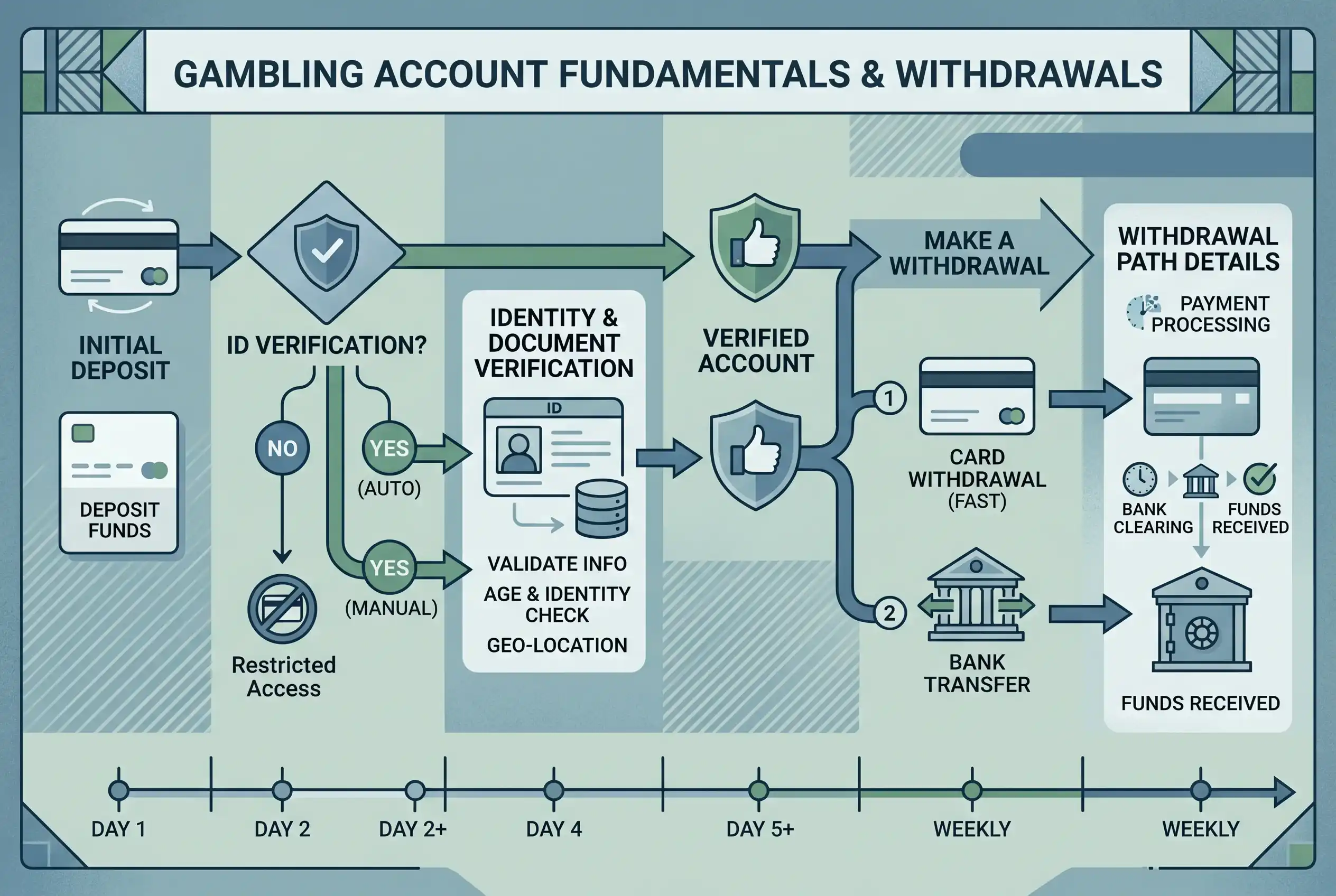

- Identify the category. Put the problem into one of five groups: payment method, age or identity, financial information, withdrawal delay, or bonus and deposit-balance wording.

- Check the official boundary for that category. For Great Britain-licensed gambling, credit-card gambling is not allowed, online gambling businesses must ask customers to prove age and identity before gambling, and financial questions can be connected to crime prevention and avoiding financial harm.

- Ask whether the request is explained. A clear operator should explain why information is needed, how it is used and what happens if the information is not provided. A vague demand for documents with no privacy or complaint information is a warning sign.

- Separate account checks from withdrawal rights. A legitimate check may need evidence, but customers should be able to withdraw money without unreasonable delay or restriction. Deposit balances should not be locked simply because a bonus is pending or active, subject to regulatory obligations.

- Keep records if the problem continues. Save the date of the request, what was asked for, what you supplied, messages sent and received, and any terms relied on by the business. If the issue is not resolved, use the complaints and dispute route.

Payment-method checks

For Great Britain-licensed gambling businesses, credit-card payments for gambling are not accepted. The Gambling Commission also explains that e-wallet funds should not be loaded from a credit card for gambling use. That boundary is important because credit gambling can make losses harder to manage and can hide the real cost of the transaction.

Be cautious with any site that presents credit-card use, anonymous payment or payment friction as the reason to join. A payment route should not be attractive because it avoids controls. If the selling point is that normal banking or identity safeguards do not apply, that is not just a convenience claim; it is a risk signal.

Do not assume that a payment method being technically available means the whole account is safe. A payment option tells you little about licence status, terms, complaints, customer-funds protection or data handling. Those checks sit on separate pages for a reason.

Age, identity and financial checks

Online gambling businesses must ask customers to prove age and identity before gambling. The Gambling Commission links those checks to age verification, identity confirmation and self-exclusion. This is why “no ID” claims should be treated carefully. They may sound quick, but they can also mean the site is not following the checks a Great Britain-licensed customer would expect.

Financial information can also be requested. Official guidance explains that gambling businesses may ask about finances to keep crime and money laundering out of gambling and to avoid customers falling into financial difficulties. In casino contexts, customer due diligence can apply to business relationships, suspicion, doubts about documents or information, and specified transaction scenarios.

A reasonable check should still be handled transparently. You should know what is being requested, why it is being requested, where to send it and how your data is protected. If the question is mainly about document safety and third-party sharing, use the ID and privacy guide before sending anything sensitive.

Withdrawal problems: what is useful to ask

| Situation | Useful question | What to record | Next step |

|---|---|---|---|

| Withdrawal has not been processed | Has the business given a specific reason and a clear next action? | Request date, amount, messages and terms cited | Ask for a written explanation; escalate if the delay remains unclear |

| Documents requested after withdrawal | Is the request tied to identity, age, financial information or due diligence? | Exact documents requested and the reason given | Check data handling and complaint information before sending sensitive material |

| Deposit balance restricted by bonus | Is the business restricting deposit funds because a bonus is pending or active? | Bonus terms, balance breakdown and withdrawal message | Use the terms and balance guide for the detailed check |

| Payment method rejected | Is the method restricted by official payment rules or by the business terms? | Payment attempt, method and rejection message | Do not seek a route around credit-card, bank-block or identity controls |

Warning signs to take seriously

- A site promotes “no verification” as a main benefit rather than explaining age and identity checks.

- A payment route is described as useful because it avoids a bank block, credit-card restriction or account safeguard.

- The withdrawal page adds new conditions that were not visible in the account terms before deposit.

- The business asks for sensitive documents but gives no clear privacy, security or complaint information.

- The site treats a bonus balance and a deposit balance as if both can be withheld in the same way without explaining the basis.

- Support replies pressure you to keep playing while a withdrawal or document issue is unresolved.

A warning sign does not automatically prove that the business has broken a rule. It does tell you that the issue should be documented and handled carefully, not solved by making another deposit or trying a different payment route.

If an operator refuses to process your legitimate winnings, you must know what to do about withdrawal, bonus or account complaints to protect your rights.

When pressure to gamble is part of the issue

If the payment question is really about continuing to gamble after a self-exclusion, bank block or cooling-off decision, do not frame the problem as finding a method that works. Payment routes, ID checks, bank blocks and self-exclusion tools are protective systems. Treating them as obstacles to overcome can make the situation worse.

Use the protection and support guide if the urge to gamble is urgent or if you are trying to continue despite a block. If the problem is an unresolved balance or withdrawal, keep the account evidence separate from any urge to keep playing.

Official pages that support these checks

- Gambling using a credit card for the Great Britain payment boundary.

- Age, ID and financial verification for age and identity checks.

- Why gambling businesses want to know about your finances for financial-information requests.

- I cannot withdraw my winnings for withdrawal-rights context.

Payment, ID and withdrawal decisions

Does an ID request always mean something is wrong?

No. Age and identity checks are part of online gambling account controls. The useful questions are whether the request is clear, proportionate, secure and linked to visible account information.

Can a business ask about finances?

Yes, financial questions can be connected to crime prevention and avoiding financial harm. That does not remove your need to check privacy, security and complaint information before sending sensitive documents.

Should I use another payment route if one is blocked?

Do not use another route to get around a credit-card rule, bank block, identity check or self-exclusion decision. If a block is active, treat it as a protection signal and seek support if gambling pressure is high.

We always advise players to choose platforms that are fully transparent, as highlighted on the NoGamStopDeposit homepage.

Creado por la redacción de «Casino not on Gamstop».